|

Taxpaids - Non-Scott-Listed US Revenues

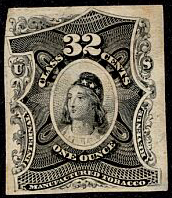

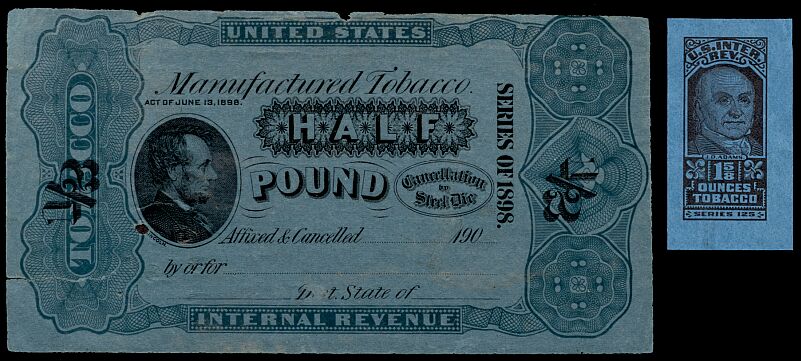

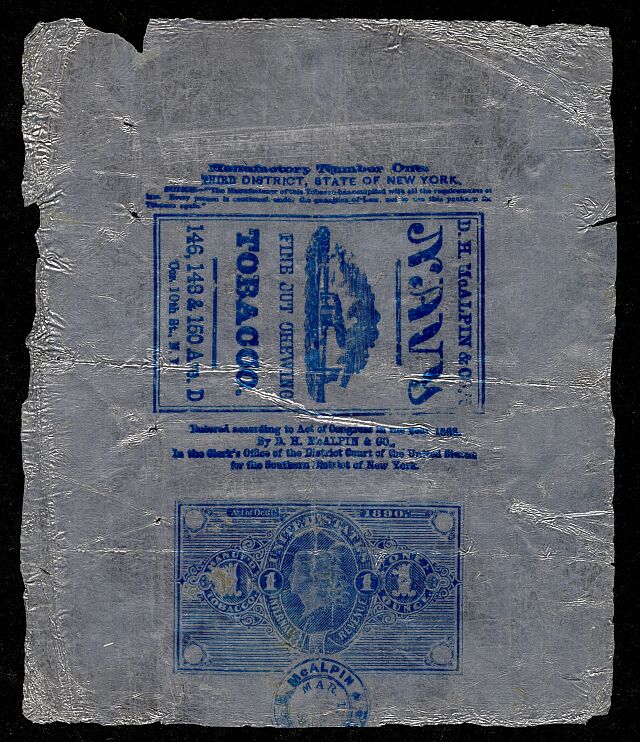

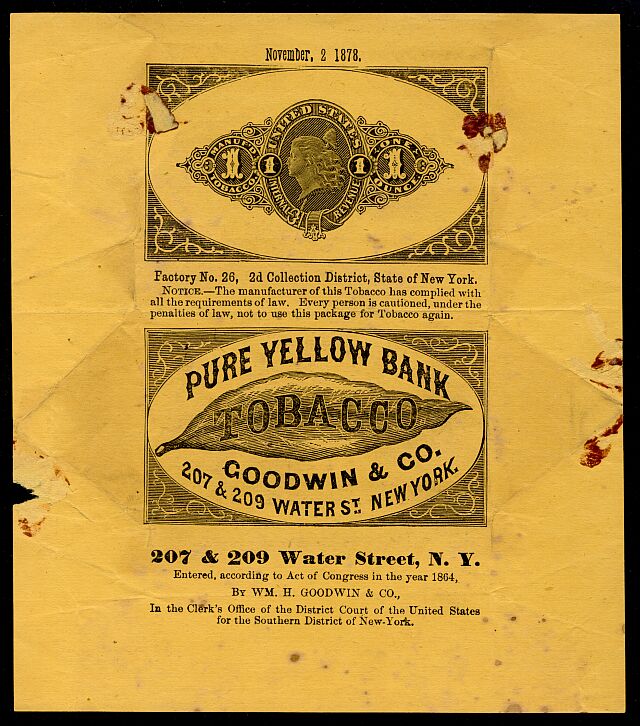

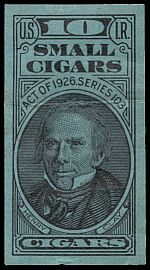

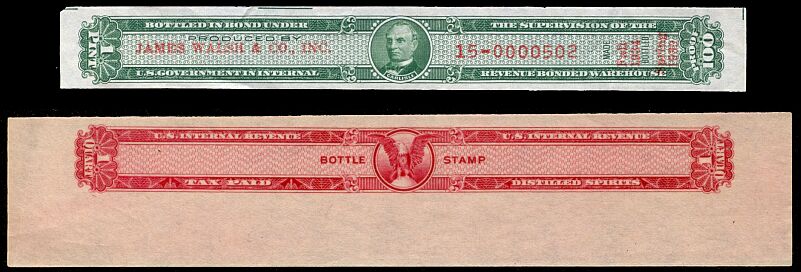

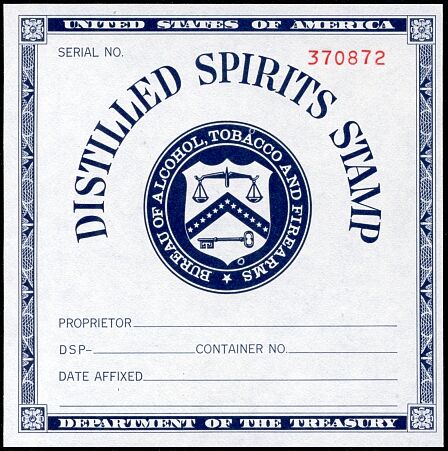

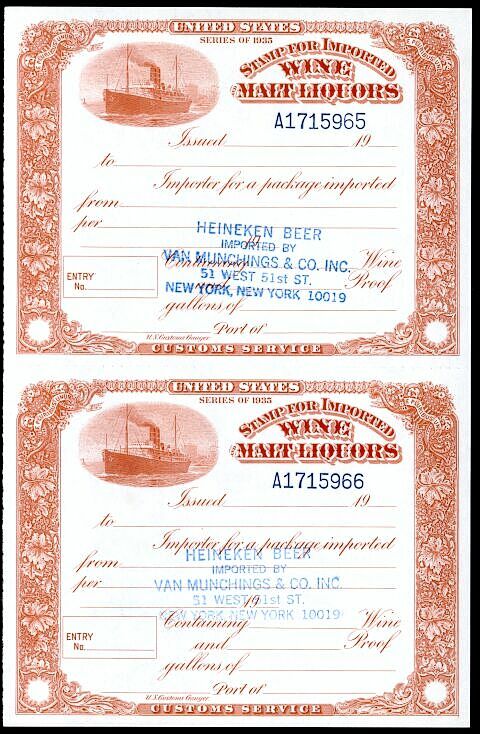

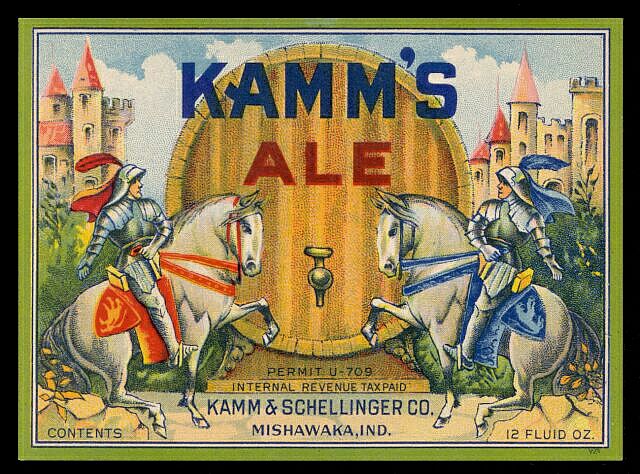

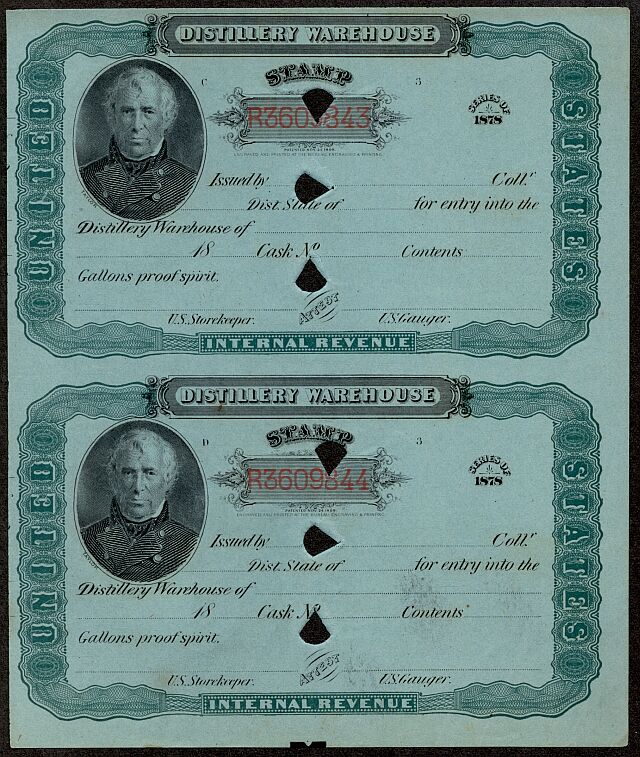

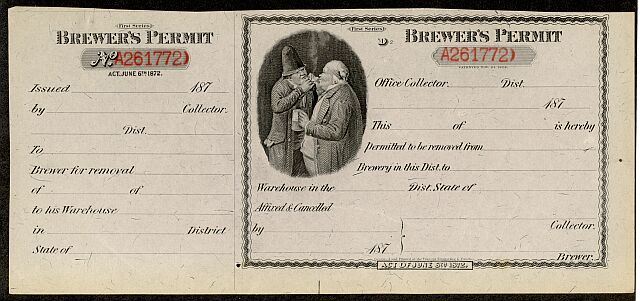

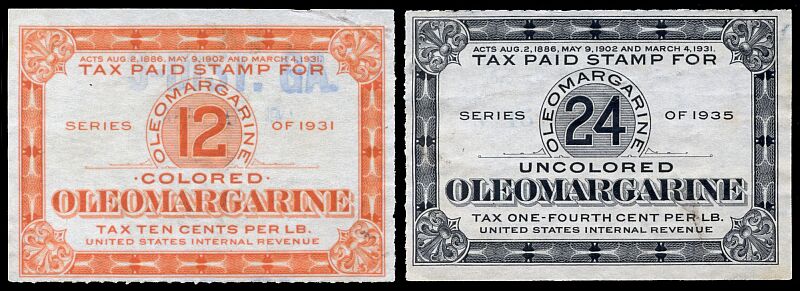

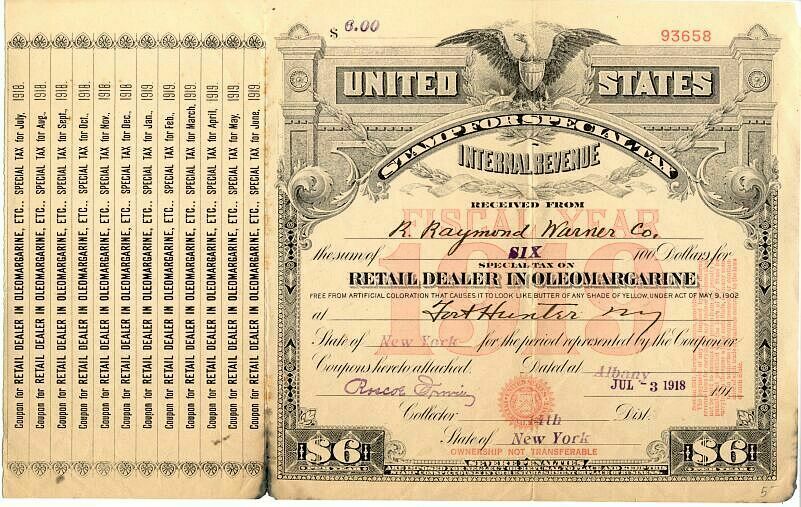

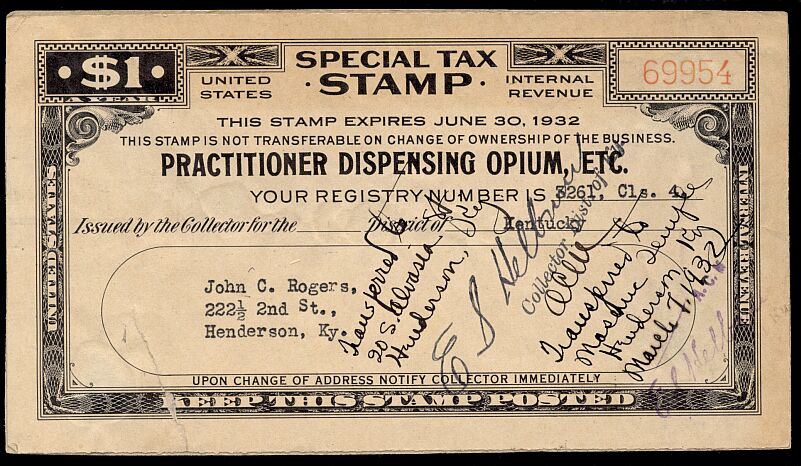

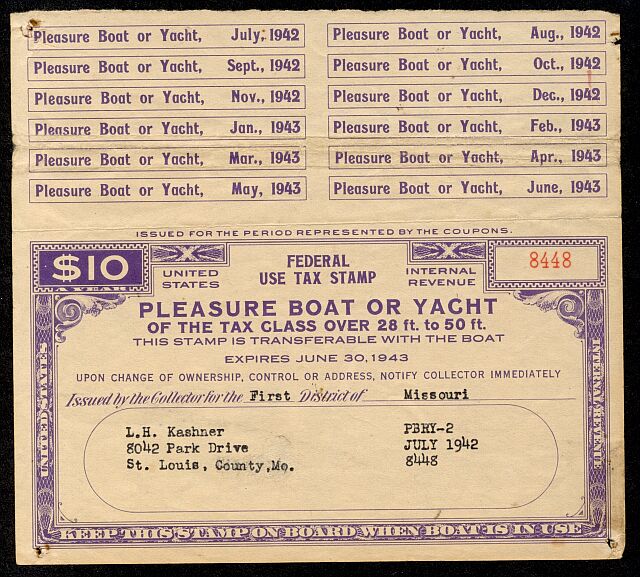

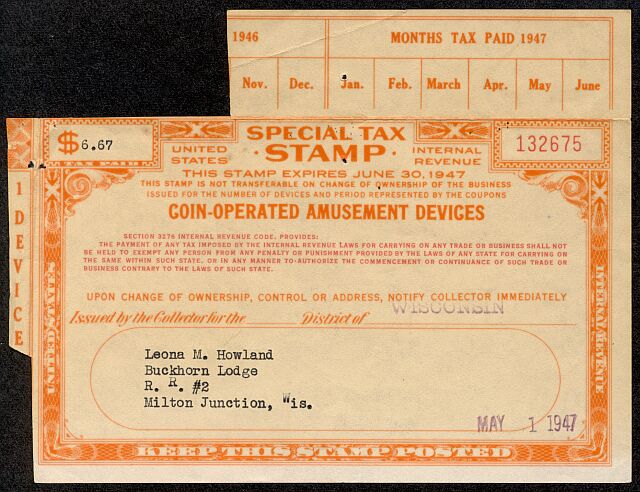

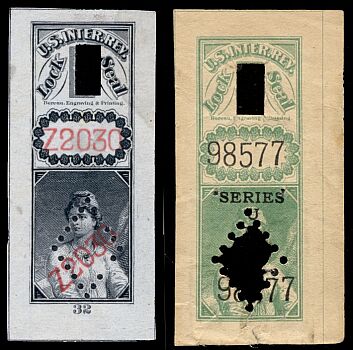

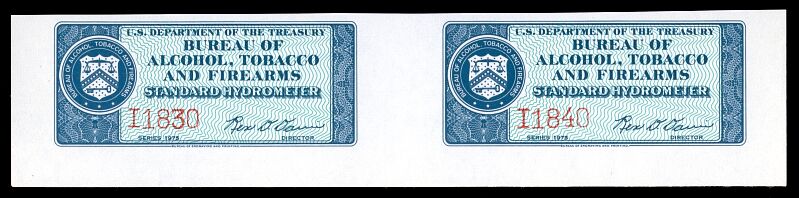

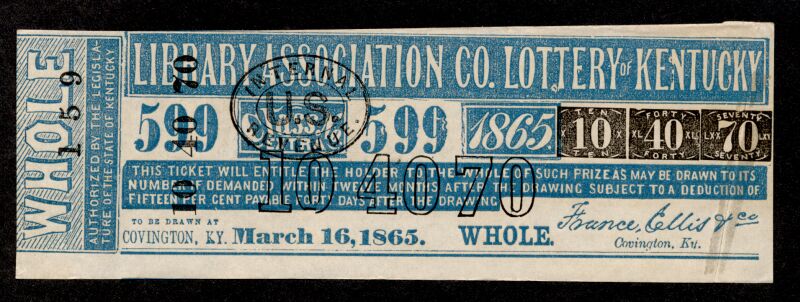

"Taxpaids" is the catchall title for United States Federal revenues that, for the most part, are denominated in units (one pint, 3/5 barrel, 10 cigarettes) rather than money. They are not listed in the Scott Specialized Catalog at present, although Scott appears to be adding some of the categories each year. Many of them are listed in the catalogs put out by the late Sherwood Springer. Many different items fall into this category. This web page is only an overview, and is an expansion of one developed for an online meeting of the eBay Users' Stamp Club. I do not actively collect taxpaids, and I have two friends who do so avidly. As you can imagine, they do not leave me with anything really unusual if they can help it. Perhaps one of them will construct an introduction that will supersede this one. Many of the taxpaids were issued to collect the so-called "sin taxes." To begin with, there are a number of types of tobacco tax stamps. Stamps were first used to show payment of taxes on manufactured tobacco in 1868. These are denominated in cents per pound - sixteen cents for tobacco with stems and thirty-two cents for tobacco without them. This is a stamp for one ounce at thirty-two cents. Stamps were printed for weights from one-half ounce to one hundred pounds. This strip stamp paying the tax on four ounces of tobacco with stems was part of the 1869 issue, and this is the stamp from the same series for sixteen ounces. Various series of stamps were produced during the 1870's, 80's and 90's, and on into the 1900's. The left stamp in this illustration was part of the series of 1898, and the right stamp is one of the John Quincy Adams type that was run in a series beginning with 110 in 1940 and continuing through 125 in 1955, with several values being used into 1958. Chewing tobacco was often packaged in tinfoil, or lead coated in tinfoil. It was possible to indicate payment of the tax on these packages with a stamp printed directly on the foil. The stamp on this wrapper used in 1890 is printed on the bottom 2/5ths. Several companies continued to use these packages with imprinted stamps through 1942. Paper wrappers with revenue imprints were used briefly in 1868 and 1878-9. This is an example used in November of 1878. The revenue design would later be used for the imprinted revenues of the Spanish American War era. From 1868 to sometime in 1870 the thirty-two cent manufactured tobacco stamps were used on snuff. After that time specific stamps were printed for use on snuff packages. Overprinted tobacco stamps were used in 1872, and then another series of snuff stamps was introduced. In this illustration the rather bedraggled stamp on the left is the four-ounce from that series. A number of other designs were used until 1932, when the tobacco plant series started. As with the tobacco stamps the first of those was series 102 and the last was series 125 used in 1955. The stamp in the illustration at right is from series 107, 1937. Cigars had their own stamps beginning in 1863. They were taxed per thousand on the value of the cigars. In 1868 the tax rate went to $5 per thousand cigars, regardless of value. This is the stamp used for one hundred cigars from the 1868 series, while this is the one from the second series of 1875. Several other series of long strip stamps followed until 1910, when smaller designs were used for most values. In 1917 the tax rates were divided into five classes depending on retail price: these were designated A through E. In 1932 a numbering system began at 102, as for the snuff and manufactured tobacco stamps. In this illustration the stamp at the left is a 1955 stamp for five cigars priced at four to six cents. The stamp at right is for fifty cigars priced up to two-and-a-half cents each, and was designated for use in 1940. Small cigars (weighing less than three pounds per thousand) were grouped with cigarettes until 1897, when they were put into a separate tax class. This is an example from series 103, used in 1933. Cigarettes had comparable stamps. For instance, in 1910 small cigars were taxed at seventy-five cents per thousand, while the stamp at the left in this illustration shows that cigarettes were taxed at $1.25 per thousand. Beginning in 1917 there were classes of cigarettes as well as cigars, but depending upon weight per thousand. The middle stamp was used for Class B cigarettes, weighing more than three pounds per thousand, and is from series 104, meaning it was used for cigarettes produced in 1934. The stamp at the right is for Class A cigarettes, the most common type. Its number of 108 shows it was issued for 1938. Imported cigars and cigarettes had different tax rates and stamps as well. This example for twenty-five cigars is from the series of 1875, and this one for one-hundred cigars is from the series of 1879. These examples are an early imported cigarette stamp from the 1879 issue and an imported cigar stamp from the series of 1910. Liquor had its own tax stamps. The beer and malt liquor stamps were once considered as taxpaids, but they are now Scott-listed. The strip stamps that were found over the tops of bottles of hard liquor are still in the taxpaid category. These examples are a used "bottled in bond" stamp for one pint of 100-proof liquor, probably bourbon, and an unused distilled spirits stamp for one quart. Some forms of these were used until July 1, 1985. This stamp is for industrial 190-proof alcohol use. The tax rate was $10.50 per gallon, with a $9 per gallon rebate upon proof of industrial usage. Used copies are known from the 1960's and 70's. There were tax stamps for imported wines and malt liquors as well. These stamps from the series of 1935 were intended to be used in paying the tax for importing Heineken Beer. There are a number of colorful labels for ales and beers that contain wording to the effect that taxes were paid according to applicable Internal Revenue Law. This may be a reference to payment of the appropriate tax by the brewery. This attractive label is an example. Other stamps were required for moving and warehousing alcohol. These are remainders, as can be told from the triangular punches, of stamps for warehousing from the series of 1878. This stamp was intended for use in taxing removal of liquor from a brewery to a warehouse, according to the Tax Act of June 6th, 1872. Finally, though it may be stretching the definition of a taxpaid stamp a bit, some collectors include the Treasury Department prescription blanks for medicinal alcohol used during Prohibition in their collections. This copy was used in Kansas City in 1924. Other items that were subject to Federal taxes from time to time include adulterated butter, process butter (rancid butter reprocessed for human consumption), mixed flour, oleomargarine (at the urging of butter producers), and filled cheese. The most common of these are oleomargarine stamps of the series of 1926, 1931 and 1935. This illustration shows a stamp for 12 pounds of colored oleomargarine from 1931 and one for 24 pounds of uncolored from 1935. These stamps were not used after 1950. This is a mixed flour stamp of the series of 1916, still on the label where it was originally used. Some of the oddest taxpaid revenues are associated with cotton. The Tax Act of 1862 included a tax of a half-cent per pound on raw cotton, and the rate was increased several times until it was repealed in 1868. Bales of cotton were required to have marks or stamps affixed to show payment of the tax. This was normally done using brass tags with long, harpoon-like shafts that could be driven into the bale. The instrument at the top of this illustration is one such revenue stamp. The other three metallic objects were used in connection with the cotton tax of 1934-36 that was part of the Agricultural Adjustment Act. The yellow tag was furnished to be used on bales at hand at the time of the act, which were tax-fee. For the next two years, until the act was declared unconstitutional, cotton farmers were given production allotments. Similar tags were attached to each bale up to the allotted amount to indicate that no tax was due on them. The unpainted one was for 1934-35 and the red one for 1935-36. The Special Tax stamps are licenses for engaging in certain activities. The very large (foot-long) unused "remainders" issued in connection with occupations such as operating a still or dealing in tobacco in 1873-85 are common, thanks to the purchase of 213 tons of this material by Hiram Deats and E. B. Sterling in 1890. These can be distinguished by triangular punches. Used copies are much less common. This is a used 1884 Special Tax stamp issued in Oregon for dealing in manufactured tobacco. The Special Tax stamps persisted into the Twentieth Century. In the early part, the stamps were still large, like this example from 1919 licensing a dealer in oleomargarine "free from artificial coloration that causes it to look like butter of any shade of yellow under Act of May 9, 1902." Later ones were smaller in size, like this one for a Practitioner Dispensing Opium, etc. from 193102. The holder moved twice in a year, and his tax stamp was endorsed by the Collector of Revenue each time. This Special tax stamp was issued for ownership of a pleasure boat or yacht for 1942-43, and this one was for ownership of coin-operated amusement devices, 1946-47. Food order and cotton order stamps were the result of programs designed to broaden certain farm markets and provide subsidies to low-income consumers. They operated in similar fashion. Welfare recipients buying orange stamps at face value were eligible for free blue stamps for half the amount spent. The programs were introduced by the Federal Surplus Commodities Corporation in 1939, and carried on by the US Department of Agriculture in 1940 and 1941 when the FSCC was merged with other agencies and ceased to exist. Some cotton growers could also earn the surplus stamps for planting smaller crops. These examples are from the FSCC period. Those issued in 1940 and 1941 contain the initials "USDA". Lock seals and hydrometer labels are not tax stamps, but were used in enforcement of tax laws and are thus considered by many collectors as part of the taxpaid field. Lock seals were inserted into special distillery warehouse padlocks to cover the keyhole and make it impossible to remove liquor without proper control and taxation. These examples show an unused and a used example. Hydrometer labels were inserted into the bulb of an instrument used to determine the percent of alcohol in a liquid and thus allow an inspector to compute the proper amount of tax to be assessed. These labels date from c. 1866 forward. This pair is from the series of 1975. Finally, a rather obscure taxpaid item, a lottery ticket from 1865 with "US Internal Revenue" stamped or printed on the face. Lotteries were taxed five percent of the proceeds in the Act of June 30, 1864. There are other types of taxpaids, and literally thousands of different varieties in the types I touched on. The Springer's Handbook of North American Cinderella Stamps Including Taxpaid Revenues is an invaluable reference - in fact, there are ten editions, but the sixth through tenth include most of the relevant material. All but the tenth are out of print, and I'm not certain about it. Introduction to United States Revenue Stamps by Richard Friedberg covers some material on taxpaids, and back issues of The American Revenuer, the magazine of the American Revenue Association, are also a good source of information. For the last several years the Scott Specialized Catalog has added one class of taxpaids each year. If that policy continues long enough this vast field will become a lot more comprehensible to many more collectors. |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}